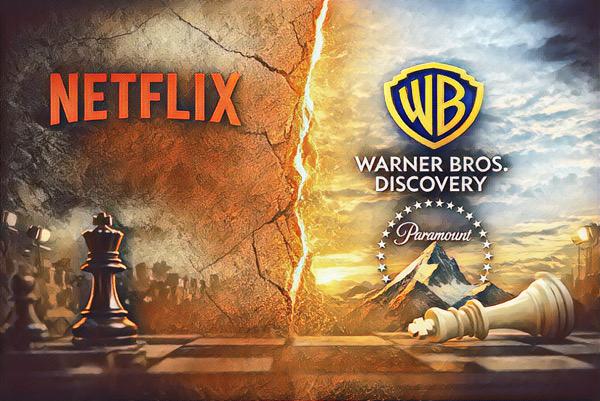

Hollywood’s chessboard shifted in a matter of days, yet Netflix’s withdrawal from the battle for Warner Bros. Discovery does not resemble a classic defeat. On the contrary, it carries the cold, calculated air of a company that decided not to overpay for something it wanted but did not need. The rival proposal put forward by Paramount Skydance was deemed financially superior, and Netflix had the chance to match it. It did not. In an industry accustomed to impulsive moves and wars of ego, the refusal felt almost disconcerting.

There is something deeply revealing in that decision. For years, analysts portrayed Netflix as a prestige-hungry company, eager to acquire a major traditional studio and cement its position as the heir to the old system. Warner, with its monumental library and global brands, seemed the perfect piece. But it was also a heavy package, burdened with debt, legacy structures, linear channels, and industrial commitments that extend far beyond streaming. By stepping back, Netflix made clear that it has no intention of turning itself into a digital version of a twentieth-century conglomerate.

The immediate reaction from parts of the industry was relief, especially among theater owners. Had Warner fallen into Netflix’s hands, the fear was that traditional cinema would lose even more ground, with shrinking release windows or direct-to-platform premieres. Under Paramount’s umbrella, the logic is likely to remain closer to the current hybrid model, in which blockbusters still rely on theaters to justify their budgets and cultural impact. In this specific sense, cinema gains breathing room. Not a guarantee of stability, but at least the feeling that it has not been completely overtaken by the logic of pure streaming.

That does not mean franchises are safe. Mega-mergers rarely preserve creative universes for sentimental or historical reasons. What prevails is mathematics. Catalogs are reorganized, divisions merged, projects canceled, and intellectual properties evaluated almost exclusively by their immediate return potential. Warner carries some of the most influential narrative assets in modern entertainment, from superheroes to literary adaptations, as well as decades of premium television. Integrating all of this into another conglomerate inevitably produces cuts and strategic realignments. For every brand strengthened, another may be quietly shelved.

There is also a less visible but perhaps more important paradox. Paramount now assumes the financial and operational risk of integrating two giants at a moment of structural transformation in the industry. High debt, overlapping teams, and the need to justify synergies often turn such mergers into long and turbulent processes. Corporate history is full of conglomerates that expanded too quickly and, years later, were forced to sell parts of themselves to survive. In that context, Netflix’s decision may look less like a retreat and more like a long-term bet.

Because the company does not need to own a studio to access its content. It can license, co-produce, distribute globally, or simply wait. If the new entity faces difficulties in the future, specific assets may appear on the market under far more favorable conditions than a full acquisition today. In other words, Netflix preserves liquidity and flexibility while another company bears the weight of integration.

There is also the regulatory dimension, often underestimated outside financial circles. A merger between the world’s largest streaming platform and one of the most traditional studios would likely face antitrust objections across multiple countries, potentially delaying or even derailing the deal. The Paramount Warner combination, though enormous, is perceived as less disruptive than the creation of a dominant super-streamer. Avoiding a long and uncertain regulatory battle may have weighed as heavily as the price itself.

Ultimately, the episode reveals a shift in Netflix’s own mindset. During its rise, the company seemed driven by continuous expansion, accumulating content and subscribers on a global scale. Today it behaves more like a mature corporation, focused on profitability and on maintaining its position without assuming unnecessary risks. This is not the posture of a company being outmaneuvered, but of one that believes it has already won the decisive phase of the streaming wars.

Whether the cinema will be safer depends on the time horizon. In the short term, yes, because it avoids a sudden rupture in distribution models. In the medium and long term, nothing suggests that consolidation has ended. The industry is still searching for scale, efficiency, and survival in a fragmented and expensive market. The Paramount Warner merger may be the end of one chapter or merely the prelude to a larger one.

And this is precisely where Netflix’s retreat takes on strategic contours. By exiting the auction without financial or regulatory damage, the company preserves the option to reenter the game in the future, perhaps not to buy an entire conglomerate but to acquire exactly what it wants when the market is more vulnerable. In Hollywood, definitive defeats are rare. What exists instead are moves of patience.

Descubra mais sobre

Assine para receber nossas notícias mais recentes por e-mail.

1 comentário Adicione o seu